Demonetisation - Why did it NOT affect GDP at all?

India released its GDP growth number for Q3 of the Financial Year 2017 (April 2016-Mar 2017) and it clocked in at 7%. This performance was particularly noteworthy (pardon the pun) because 86% of notes in circulation were withdrawn on November 8. The problem eased only by mid-January. Thus, two out of three months in the quarter, India faced a massive disruption. Anecdotally, during the period since November 8, most of the country was busy depositing cash, swapping notes etc. Consumption activity was reduced, there was stalling of transportation services (trucks) etc. Experts commented that Indian GDP growth would reduce - by 1.5-3% from ~7.5%. In effect, markets were expecting GDP to clock in at 6.1%. Notwithstanding that, Indian GDP came in at a strong 7%. Economists were spooked and people have started blaming the CSO for the quality of data.

Naturally, today's papers are filled with sceptical articles.

Mint Manas Chakravarty concludes that this is not entirely because of base effects. In fact, some sectors have had base effect advantages but others do not. Overall, the trend in activity seems to be smooth.

Another Mint article indicates a possibility that Strategic timing of demonetization and fiscal stimulus seems to have helped in retaining growth despite demonetisation. Here the author suggests few reasons. First, the informal sector mainly affected by demonetization is not appropriately captured in GDP statistics. It also attributes the muted impact to strategic timing after the festive season demand has played out. The Third reason could be that the government has been using some sort of a counter-cyclical fiscal policy to stimulate investment activity. Government Final Consumption Expenditure (GFCE) grew at a massive 19.9% in year-on-year terms in the previous quarter.

The Economic Times questions the credibility of the data. In another article ET cities various analysts /economists who find the data incredulous. Interestingly, ET also has an article that says Fiscal deficit for first 3 quarters has surpassed the annual target. This sort of corroborates with the Mint's suspicion of fiscal stimulus.

Financial Express article states that, some analysts believe that some said use of old notes for consumption might have contributed to the rise. It also highlights some discrepancies —

the difference between the supply and demand side of GDP — turned negative after a gap of four quarters (-Rs 6,767 crore) in the December quarter, compared with Rs 45,378 crore in the second quarter and Rs 30,645 crore in the first quarter. In the last quarter of 2015-16, discrepancies touched a massive Rs 1,43,210 crore, causing a flutter then and raising doubts about the credibility of the country’s data collection mechanism. When private final consumption expenditure, gross fixed capital formation, government final consumption expenditure, change in stocks, valuables, and net exports exceed the overall GDP (based on the supply side data), discrepancies turn negative.

So what happened? Was the pain felt during the demonetization unreal? Actually, no. The answer to the positive surprise in the GDP figures is in the details.

First, the informal economy is severely under-represented in the GDP numbers. Naturally, it does not count the upside nor the downside. Thus, GDP number remains disconnected from their reality. However, this may not fully explain the upside surprise.

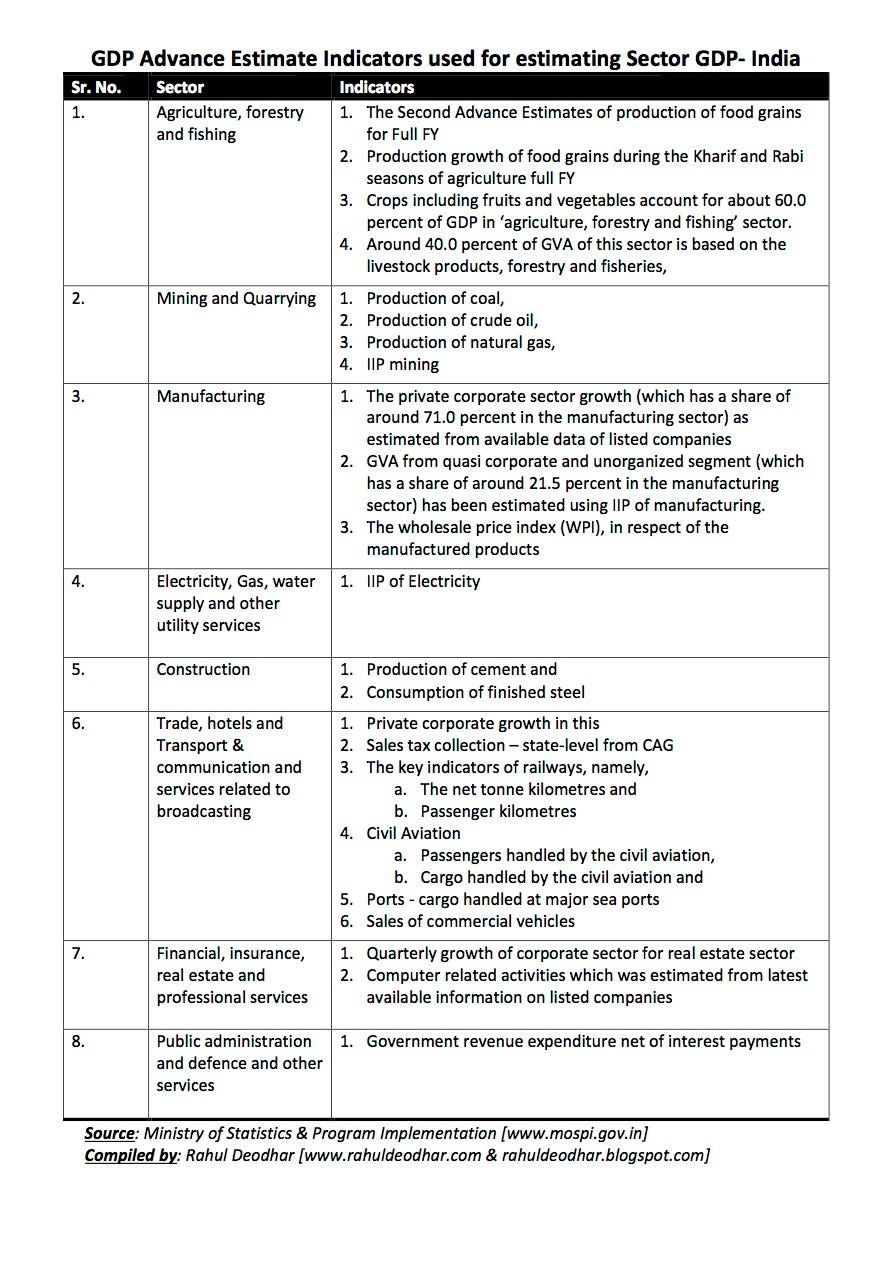

The main reason why data surprised because of the way it is designed. Nothing wrong with the calculations but these are design flaws. Here is a table showing the components used to determine the growth in individual sectors.

GDP Advanced Estimates - Indicators used for estimating GDP

If you notice, the indicators are not sensitive to the demonetization effect. At least not so quickly. The effect of using these indicators is that you will get a smoothened GDP series when compared to changes on the ground. Most of these indicators were positively affected by demonetization. For example,

More taxes (municipal, sales and excise, etc) were paid so as to use the existing cash.

Many smaller firms were used to push money into bank accounts by showing that as cash sales (taxed at 35% v/s penalty rate of 50%).

Agricultural sowing/production was not affected because of the timing of the move.

The number of train bookings had gone up during the demonetization period. There could be a similar increase in freight bookings too.

All in all, I do not think it is any calculation or manipulation effect. The high GDP number is result of design of the indicator itself which leads to smoothened output. Naturally, we may see a dampening effect in subsequent quarters are the true distortion gets dissipated.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".