Killing Savings made homes unaffordable

Savings was easy in era of gold money. When government moved to fiat money they made a promise to the savers. That promise is broken. So now housing is unaffordable. How? Let us see.

Saving is one of human society's core values. Maybe we learnt it from the Ants, unlike the grasshoppers. Or maybe when “woods we passed, we saw the squirrels hide their nuts in the grass”. However we leart it, saving has allowed for all the progress we see today.

Savings were easy in the era of gold money.

It was as easy as hiding your money under the mattress. The money won’t lose value. It was fool-proof if you could protect your money.

Soon, we moved to gold-backed money. Here, our paper money was equal to a certain amount of gold stored in the local bank. We could go right to our bank (usually also goldsmiths) and get our gold. We even bit the gold to check if they gave us the real deal.

Then, we entered the era of regulated banks! Our gold went from local banks to central bank vaults - those in London and Fort Knox in the US. The money was still marked in terms of some weight of gold, but only difference was that we could not get our gold from the bank. Rather we could buy gold from gold-smiths who now were jewellers.

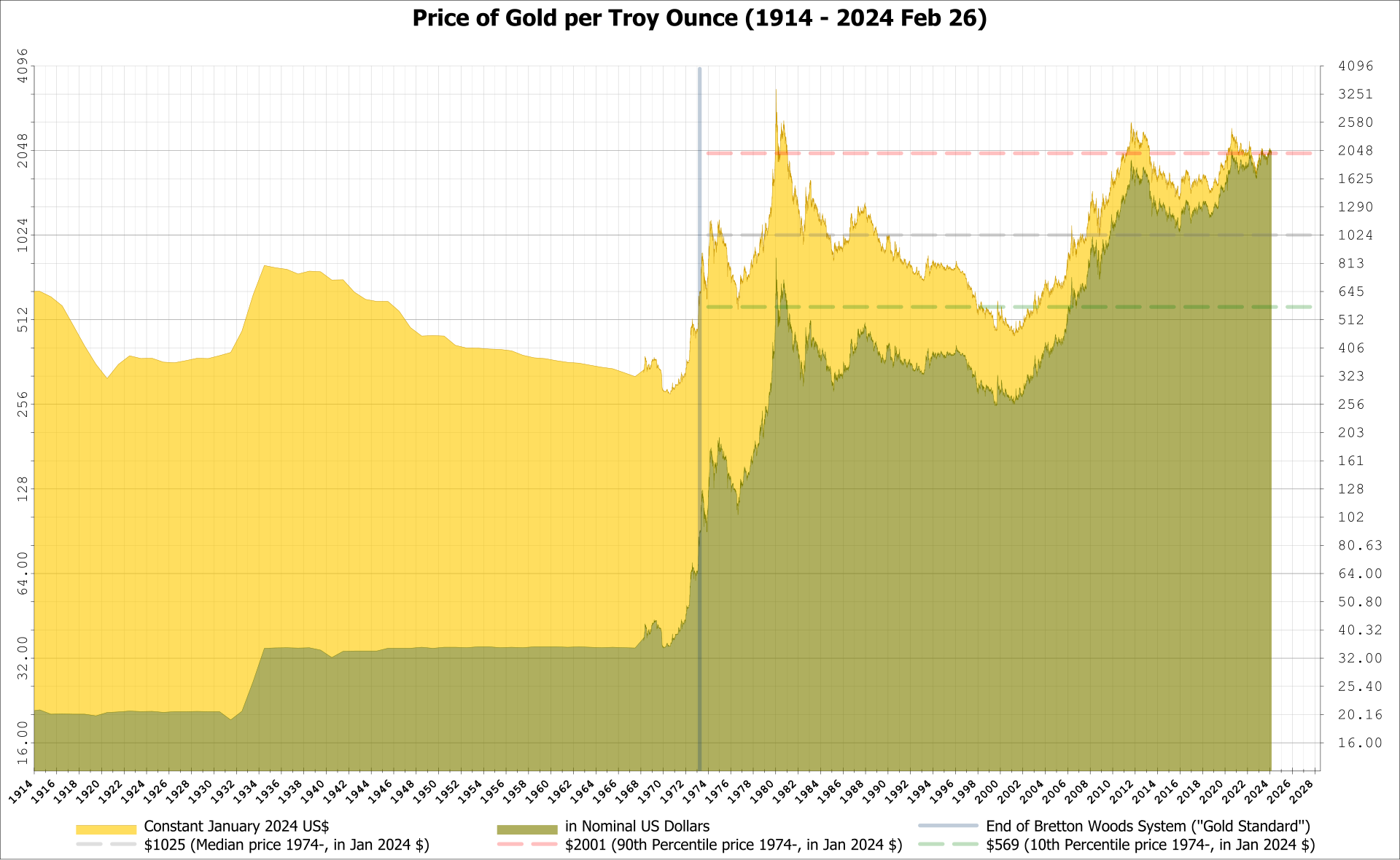

In each of these changes, the weight of gold is reduced. In other words, earlier, we were holding Gold coins. Then, we moved to gold-backed money, and we fixed the price of gold in dollar terms. That rate was lowered slowly (less gold per dollar) until, in 1974, the gold standard was abandoned, and the government moved to fiat money.

The story is that the US Government realised that it had printed more money than the amount of Gold it had in the vaults. No one realised as everything was working just fine; till someone did! Some European countries were holding a lot of US dollars. Some of them, particularly France, realised that the Gold equations do not tally. So they asked the US Government to send them the Gold instead of US Dollars. Other European countries woke up. And that was the end of that.

The US Government went into a panic and, as it usually does, screwed a few countries. US Treasury Secretary John Connally said emphatically - “My view is that the foreigners are out to screw us, and therefore, it's our job to screw them first!”

Normal people wondered how much their money was actually worth in gold terms. That led to a new concept entering the public discourse—inflation, the rate at which money loses value. But normal people were not happy. The normal people were livid. They started the campaigns like “Government is taking our money” and “The government is cheating our savings from us”.

So, the government made a promise to the savers.

The government promised that the inflation rate would be below 2%. They even passed a law saying the US Fed would keep inflation in check and restrict it to 2%. The savings rate was never below 3% (except during World War). This would keep the cost of living from rising more than 2% every year.

So this was the deal. We keep our money in the bank, and it actually appreciates in value rather than staying under our mattress and holding value. If we let banks invest it on our behalf, we get more returns on our money, and the banks will return ALL our money when we want it. You would earn a higher-than-inflation return at a very low risk.

This was a promise to the savers.

That promise has been broken.

Today, earning higher-than-inflation returns at such a low risk is impossible.

The government has broken the way we measure inflation. The inflation today does not reflect the real cost of living. The government says it's 2% or 4%, but in real life, it feels more like 6% or 8% or even more! So we need to earn at least 8% to keep the purchasing power of our savings intact. But the best we can earn with low risk is 4-5%. To earn the additional 4-5% we have to take higher risks.

But the government has broken the way we measure risk too. So to earn a return of 8-10% we end up taking very high risks whereas Globally Systemically Important Financial Institutions (G-SIFIs) can aim for returns of 15-20% easily and if they fail they get bailed out!

So normal people started hiding their money - in homes!

Since you can’t hide paper money under a mattress, you have to invest it somewhere. That was housing. As people earned, they bought houses. Some bought many houses while others bought bigger houses. As a result, housing prices rise.

As housing prices rose, so did rents, fueling inflation. Then, central banks remembered their promise of 2% inflation and jacked up interest rates. Guess who it hurt the most? The poor! With high interest rates, economic growth was squeezed, salaries stagnated, mortgage payments rose, and housing became even more unaffordable.

This created a positive spiral for housing. People started noticing and believing that “house prices never go down.” Thus, a housing boom like no other began. Today, corporates and hedge funds make many housing investments. Today, Blackstone is the biggest landlord in the US. The result is that now housing is unaffordable.

In Sum

The lack of regular, reasonable and low-risk returns has led many to invest in property markets. The resulting frenzy has made homes unaffordable. It leads to late household formations, fewer kids per household and population implosion. It also INCREASES the cost of raising kids and thus makes population growth very hard.

It also created a negative spiral for lower-income households. Whenever inflation rises, central banks slap the economy hard on the face of lower-income households, squeezing their income and prosperity.

We need to rethink our promise. The money contract between the state and the people needs to be renegotiated.